LPSN’s trials and tribulations started in 2021. Once seen as a growth stock on the back of the company’s early adaptation of AI in its customer engagement platforms, the shares suffered a brutal rerating when the promised growth failed to materialize: having peaked at $1,071 five years ago, they now trade for less than $3.

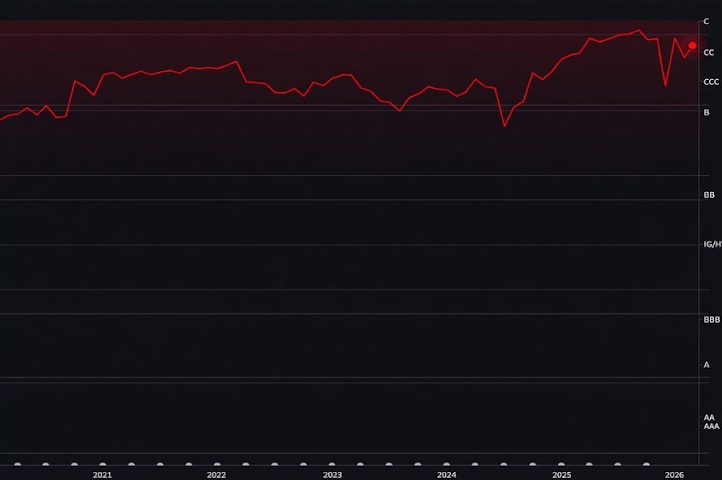

The company’s credit risk rating, as calculated by AIR’s AI-powered intelligence engine, did not succumb to the same irrational exuberance as the equity market - AIR’s Risk Score was at the CCC-equivalent level when the stock reached its high, and has remained elevated ever since.

AIR AI-detected structural weakness

What drove AIR’s correct assessment of Liveperson’s credit risk? It wasn’t the collapse of the share price - the Score was elevated well before this occurred, and in any event a firm’s equity price is not a driver of the model. Rather, the Risk Score reflected the company’s lack of growth (quarterly revenues are now at the same level as in 2015), combined with higher debt, negative cash flow from operating activities, and at best breakeven operating profits. In short, LPSN’s history appears to be one of using debt to finance operations and to fund growth, a strategy that in this case failed to generate the hoped-for levels of earnings and cash flow.

Creditors no doubt hoped for relief from the September 2025 refinancing. Unfortunately, AIR’s analysis indicates that this is unlikely to be forthcoming. After rallying briefly and modestly, the Risk Score has returned to its former CC to C equivalent level.